Property

Our personal finances are so impacted by property, whether that is owning your own (with or without a mortgage), renting, or just the general costs of running a home! It’s likely the biggest lifetime expense you will have.

Here we will focus mostly on property ownership, specifically buying via a mortgage, and answer some of the main questions that arise through this process.

Contents

What is a Mortgage?

A mortgage is a loan to purchase property or land.

Instead of paying for the full value of a property upfront, a mortgage can be used to cover the gap between what you can afford as a deposit (an initial lump sum of money) and the value of the property.

Worked Example

Property value = £200,000

Deposit = £40,000 (which is a 20% deposit of £200,000)

Mortgage = £160,000

Useful Links

Money Super Market – Compare mortgages

Money Super Market – Top 10 tips for getting a mortgage

Money Saving Expert (warning: this is a 53-pager!)

Initial costs to buy a property

These are mainly:

- Mortgage deposit;

- Stamp Duty Land Tax (SDLT); and

- Other related costs & fees.

1. Deposit

Property price x deposit percentage %

Eg £200,000 x deposit of 20% = £40,000

The higher the deposit percentage, the better interest rate a lender is likely to offer you.

The minimum deposit depends on the lender, but can be anything from 5% upwards.

2. Stamp Duty Land Tax (SDLT)

The property buyer in the UK pays Stamp Duty in a property sale transaction.

For first time buyers there’s good news. Up to a purchase price of £300,000 you don’t pay Stamp Duty hoorah!

The rates otherwise are:

See the chart below for the different levels of SDLT incurred depending on your circumstances:

3. Other related costs & fees

The deposit and SDLT are the “fixed” costs of getting a mortgage.

Other “variable” costs include the following:

- Mortgage fees & charges – these will depend on the lender, but can often be added to the mortgage amount.

- Broker fees – depending on whether you do or don’t use a broker.

- Valuation fees – the lender will want to check the value of the property you are buying.

- Survey costs – if an older property you’ll likely need more extensive surveys to check the general state of the property before buying it (Zoopla have a good description of the different types of surveys here).

- Conveyancing fees – this is normally your solicitor, who will handle all the legal stuff!

- Moving costs – optional, depending on how much large furniture you have vs what can be moved in the car. Which? estimate these costs to total anywhere between £1,000 and £6,000!

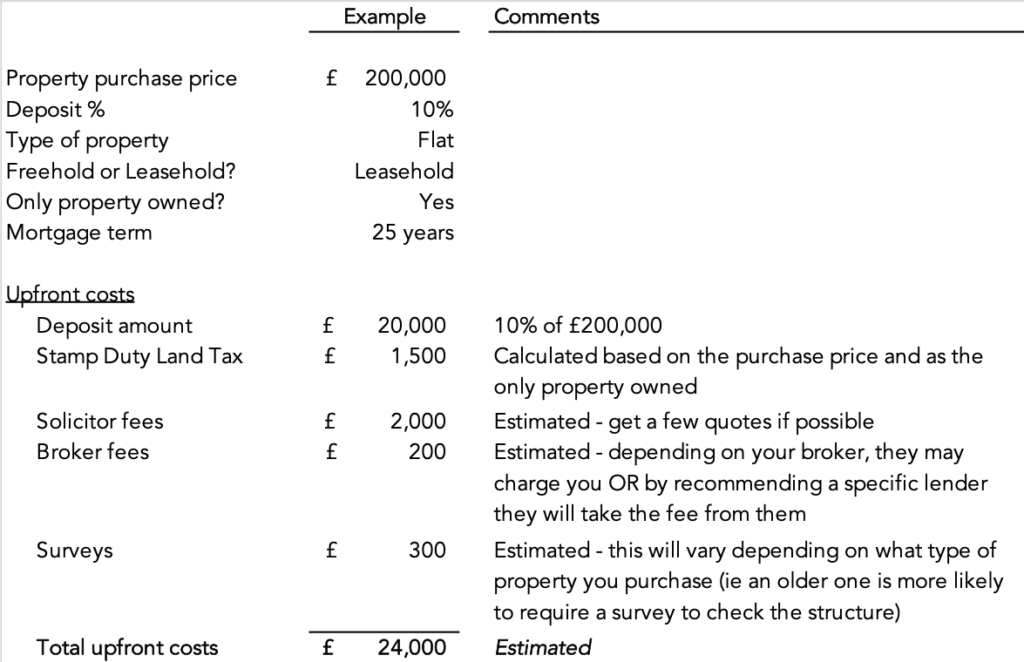

Worked Example

Note that if you were a first time buyer, the Stamp Duty Land Tax cost here would be ZERO, as the property is less than £300,000.

Useful Links

Always check the UK Gov website for the latest SDLT rates.

Money Super Market – for a quick mortgage monthly payment estimate.

Money Advice Service – a neat stamp duty calculator tool you can use to try any other values.

What Mortgage can you afford?

There are the upfront costs to consider (covered in the section above), as well as ongoing costs, which we’ll cover here.

What monthly mortgage payment can you afford, as well as all the running costs of the property?

Available income

Firstly, you’ll need to work out how much income you have available on a monthly basis after any other non-property related costs have been taken into account (eg phone bill, car lease etc).

Ideally you need to set a Budget, but just having your monthly net income (ie the amount that comes into your bank account each month) is a good start, as you definitely don’t want to exceed this!

Monthly mortgage

Next for the monthly mortgage amount, Money Supermarket has a really quick tool that you can use to calculate those monthly payments.

Your monthly payment will depend on how much you are borrowing, for how long, and the interest being charged by the lender.

There are 2 main types of interest:

- FIXED – the percentage interest charged is fixed for an agreed period (eg 3-years), so your monthly payments are the same.

- VARIABLE – the percentage interest charged is linked to the Bank of England base rate (which can change), plus an agreed fixed percentage, eg base rate + 2%. So, your monthly payments can also fluctuate.

Running costs

Finally for running costs of the property, check out the Budget section within Money Management to project what your monthly expense would be. For example you would need to take into account (not an exhaustive list):

- Utilities (gas, electricity, water)

- Council tax

- TV licence

- Home & contents insurance

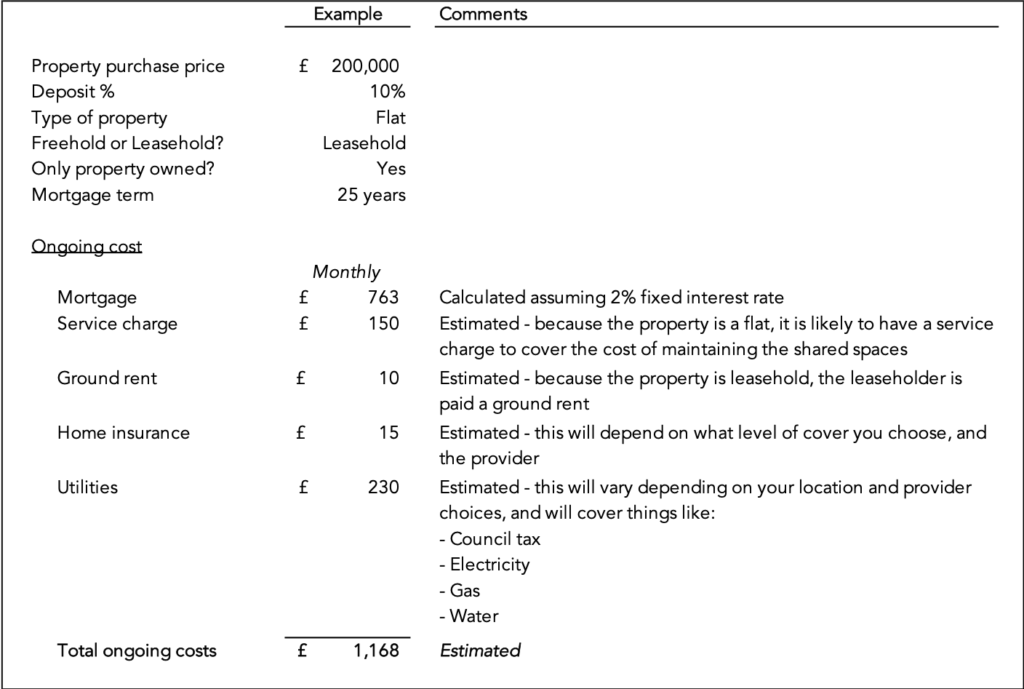

Let’s use the same information as above for the worked example.

Worked Example

Useful Links

Reminder of the mortgage calculator from Money Supermarket.

How much will the bank lend you?

Typically this is capped at 4.5 times your income (though this varies depending on which website you read!).

The Money Advice Service have a quick calculator you can use to estimate a lower and upper borrowing range.

The best way to know exactly how much you can borrow is to get a Mortgage Agreement in Principle from a lender. This is an upfront indicative decision of how much they will lend you, and nowadays is often required before you can put in an offer on a property.

Get this by essentially starting the property purchase process – you don’t need to have found a property you need to purchase to start.

Find a mortgage yourself (and apply directly to the lender) using a site such as Money Super Market; or use a mortgage broker (again you can search online, or ask family/friends for recommendations).

Check out the next section to determine whether you want to use a Mortgage Broker or not.

Useful Links

Reminder of the affordability calculator you can use from the The Money Advice Service.

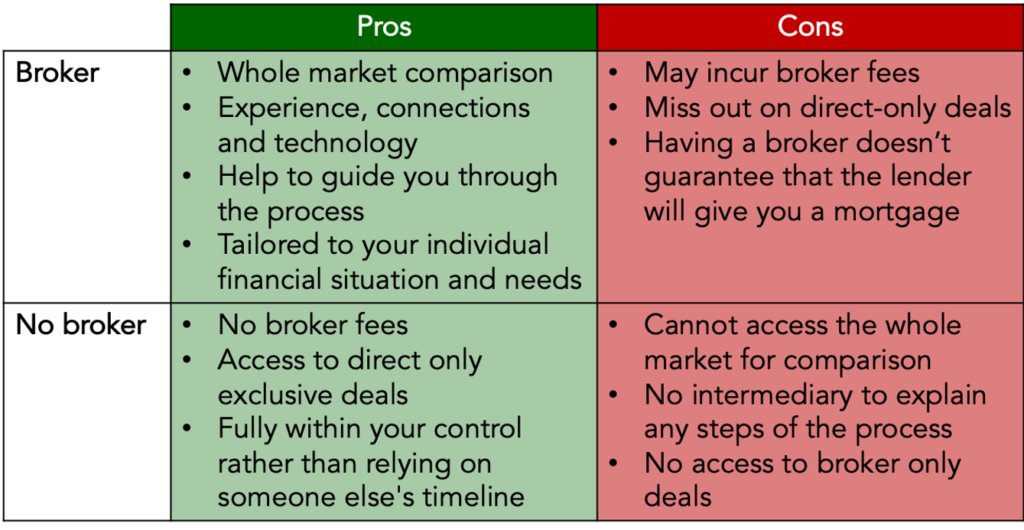

Should you use a Broker to get a Mortgage?

A broker is a person or firm who arranges transactions between a buyer and a seller for a commission when the deal is executed.

A good mortgage broker is one who gets you AND themselves the best deal!

Useful Links

One of the UK’s largest Mortgage Broker is London & Country.

Documents you need to apply for a Mortgage

When applying for a mortgage, expect to have to tell the lender pretty much everything about yourself except your shoe size.

The lender (typically a bank) want to make an assessment of whether you will be able to afford the mortgage (which to be fair, is no bad thing), to minimise their risk in lending you the money.

You’ll need to provide the following as a minimum:

- Full name

- Date of Birth

- Current address (and month/year you moved in)

- Addresses for the last 3 years (if not the same as your current address)

- Confirmation you’re on the electoral roll at current address (click here)

- National Insurance number

- Proof of deposit dated within 1 month (eg bank statement)

- Proof of ID (eg passport)

- Proof of address x2 (eg driving licence, recent utility bill)

- Your employer (company name & address)

- Date you started working for current employer

- Monthly gross income

- Last 3 months payslips (to prove you have the income you say you do!)

- Your latest P60 (get this from your employer)

- Planned retirement age

- Any debts you have (eg car leases, credit card balances, student loan etc)

- Main outgoings (eg utility bills, council tax, insurance etc)

- Last 3 months of bank statements (to show the above outgoings)

If you own a rental property, you will also need to provide:

- An Assured Tenancy agreement demonstrating the monthly rent amounts being paid into your bank (linked to bank statements above); OR

- If not currently rented but you intend to do so, you will need a signed letter from a letting agent with their rental valuation estimate.

Useful Links

Money Advice Service – How to Apply for a Mortgage.

The importance of a good credit score

The better your credit score, the more likely a bank will want to lend to you!

A credit score is your historical finance footprint, and looks at things like eg whether you have ever missed any credit card payments.

As part of applying for a Mortgage, this will be something the lender checks to determine if you are likely to repay your mortgage each month!).

Make sure you’re registered on the electoral roll to your current residence (link to electoral roll here) as this also forms part of the credit check to validate your existence as a UK citizen!

Useful Links

Money Advice Service – improving your credit score.

Re-mortgaging

Re-mortgaging is simply moving from one mortgage to another, on the same property.

Summary

When you get to the end of your mortgage term (eg at the end of a 2 year fixed agreement), you are able to re-mortgage.

There is nothing to stop you switching to a completely different lender when you re-mortgage. Your current lender is likely to contact you near the end of your agreement hopefully offering you updated terms, but it’s always worthwhile shopping around.

You can usually change the lender, interest rate, mortgage amount AND mortgage term at this stage.

Early exit penalty charges

If you re-mortgage BEFORE the end of a fixed term agreement, expect to pay early exit penalty charges. This is typically a percentage of the mortgage balance remaining (that may reduce the closer you get to the end of the fixed term), that the lender charges essentially to stop you constantly switching to the cheapest rate on offer.

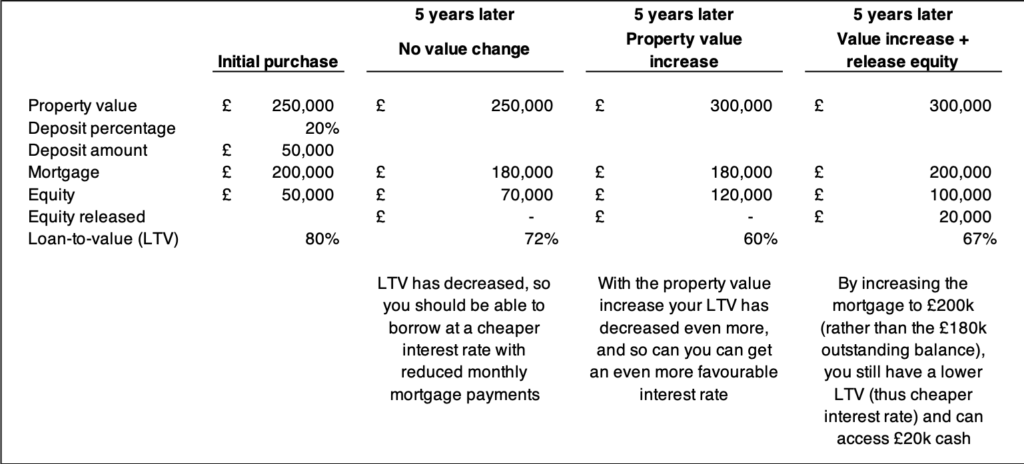

Why re-mortgage?

This is the opportunity to either:

- Reduce your monthly payments – to do this you can either decrease the total mortgage amount, extend the mortgage term or find a mortgage at a lower interest rate.

- Take some “equity” (cash) out of the property – you may be able to access some equity of the property, which essentially means getting some cash back (eg to do some renovations). The same affordability checks apply, as your mortgage monthly payments may even increase. See the worked example below.

Useful Links

Try this re-mortgage calculator from Mortgage Savings Expert.

Further reading

- To explore Overpayments, try Money Saving Expert’s mortgage overpayment calculator here.

- Halifax – overpayment calculator with a neat graph.

- Which? have a good article with more information here on applying for a mortgage if self-employed.

- If you’re not interesting in buying property and instead looking to rent, see this How to Rent guide from the Government.

- Uswitch lets you compare mortgages specifically for shared ownership.