Personal Tax

I know, the word tax hardly evokes feelings of passion and excitement. Some of it is complicated, but some of it really isn’t (promise).

This section focuses on PERSONAL tax, not company tax, which has different rules.

Note – this section reflect 2023/24 rates, which change each tax year starting 6th April (so, rates here are tax year starting 6th April 2023).

Contents

Income Tax

Income tax is charged in the UK on your taxable income.

This might come from being employed, rental income and/or savings interest.

Personal Allowance

£12,570

If you earn up to £100,000 you are eligible for the personal allowance amount of £12,570.

This is deducted from your earnings before tax is applied, ie you don’t pay tax on the first £12,570 you earn.

If you earn over £100,000, you lose £1 of your personal allowance for every £2 over that £100k mark (see examples of this below).

Basic Rate

20%

Assuming you get the £12,570 personal allowance, you will pay tax at a basic rate of 20% on earnings from £12,571 to £50,270 (ie a banding of £37,700).

Higher Rate

40%

Again assuming you get the £12,570 personal allowance, you will pay a higher rate of 40% on earnings from £50,271 to £125,140.

Additional Rate

45%

Any earnings above £125,140 will attract a tax rate of 45%.

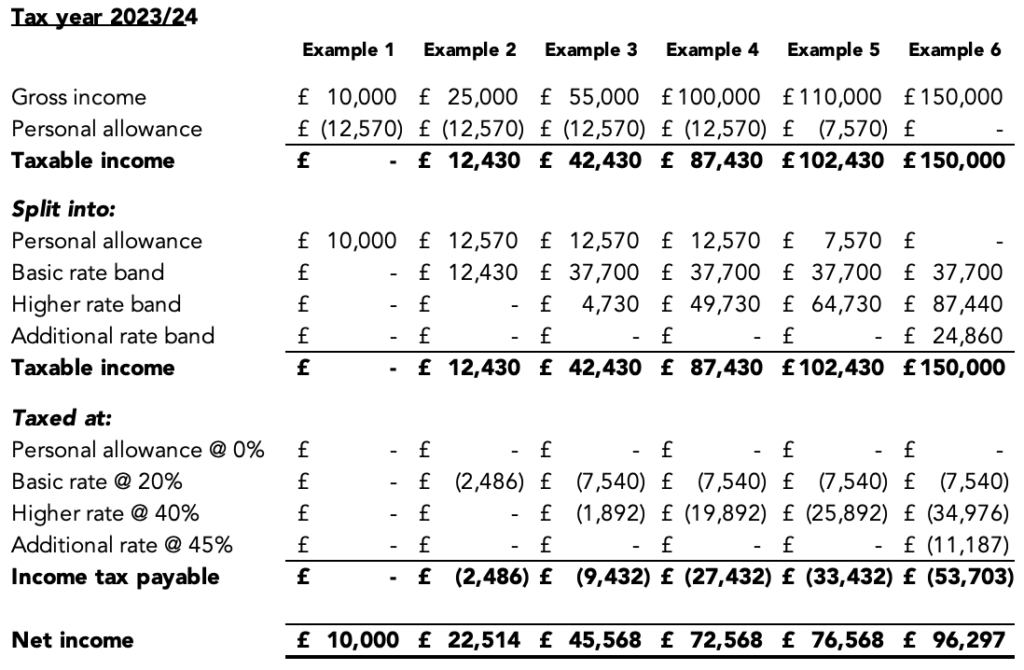

Worked Example

See in Example 5 how the personal allowance is reduced:

- Gross income is £10,000 over the £100,000 threshold

- £10,000 / £2 = £5,000 of personal allowance lost

- £12,570 – £5,000 = £7,570 personal allowance remaining

The workings above is before National Insurance is deducted, and does not take into account pension contributions – see Pension impact on Income Tax below.

Useful Links

The GOV.UK website is obviously a key source on this, as they’re the ones that tax us!

Money Saving Expert also has a good income tax calculator tool.

National Insurance

National Insurance (“NI”) in the UK funds certain benefits and the state pension.

An individual pays NI contributions to be eligible for these benefits (if needed) and the state pension.

Every person has a unique National Insurance number.

This is an NI numbercard – make sure you keep this safe!

How is it calculated?

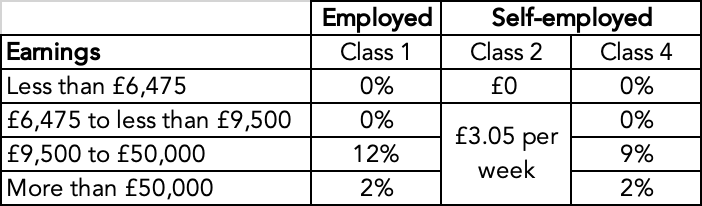

Much like income tax, it’s calculated based on your level of earnings, but varies if you are employed vs self-employed.

(Ok we’re going to cheat – TaxScouts have got an online calculator that you can input earnings to auto-calculate your NI, and also shows you how the number is calculated!).

Rates

Worked Example

- Annual earnings of £60,000, employed

- Class 1 only NI payable by you

- 0% up to £9,500 = £0

- 12% on £9,500 to £50,000 = £4,860

- 2% on £10,000 (£60k – £50k) = £200

- Total NI = £0 + £4,860 + £200 = £5,060 per annum (= £421.67 per month)

What’s the NI link to Pensions?

The main thing to note here, is that in order to qualify for the FULL state pension, you need to have made 35 qualifying years* of NI contributions (and a minimum of 10 years to get anything).

*This is a tax year (ie 6 April to following 5 April) of the correct NI contribution paid per the workings above. Check your NI record here to see how many qualifying years you currently have.

NI contributions cover:

- Contribution-based Jobseeker’s Allowance

- Contribution-based Employment and Support Allowance

- Maternity Allowance

- Bereavement Support Payment

Useful Links

GOV.UK – the ones we’re paying NI to!

Check your state pension age here.

Capital Gains Tax

Capital gains tax (or “CGT”) is tax on the profit when you sell (or ‘dispose of’) something (an ‘asset’) that’s increased in value.

The gain is what you are taxed on, and this may not simply equal the profit made (see below).

Note the terminology ‘dispose of’ means in the context of CGT either to:

- Sell;

- Give away (or transfer to someone else);

- Swap; or

- Get compensation for it (eg insurance payout if damaged).

The key exemptions to CGT (ie for which you can ignore CGT) are:

- Your main (residential) home

- Your car

- Personal possessions worth less than £6,000

For most people this covers the main assets you own and are likely to sell – phew!

Let’s start with some key things to know on rates and allowances:

- As with personal tax, the rate of CGT you pay depends on whether you are a higher rate or basic rate taxpayer for income tax (see Personal Tax section above).

- The CGT rate is different (higher) if your gain is on property (that isn’t your main home).

- You don’t pay CGT on the first £6,000 of gains (in tax year 2023/24).

Worked Example

Selling an antique cabinet:

.*Assume the seller here has used up their CGT annual allowance for the tax year.

Worked Example

Selling a 2nd property:

Personal possessions (eg antique cabinet example above) = 10%/20% for basic/higher rate tax payers respectively.

Property = 18%/28% respectively.

Also notice that the profit doesn’t always equal the gain, as there is the annual allowance to consider first and other allowable expenses you can deduct.

These can be found on the GOV.uk website as follows:

- If the asset being sold is property (if NOT your main home).

- If the asset being sold is a personal possession.

Useful Links

Check the Government website GOV.uk for the latest rates.

How do Pensions impact Tax?

When you make a Pension contribution (eg each month via your payslip), it REDUCES the amount of income on which you are taxed.

Reduce tax paid now, and pay (potentially less) later

- Pension contributions are directly linked to your taxable income – whatever you pay toward your Pension now, you are NOT taxed on.

- Then, when you withdraw the Pension later (in retirement), you are taxed on your Pension income as per the Income Tax section above.

- If you are a higher rate tax payer now (taxed at 40%), you are likely to be able to withdraw your Pension at a basic rate (taxed at 20%), ie a reduced tax rate.

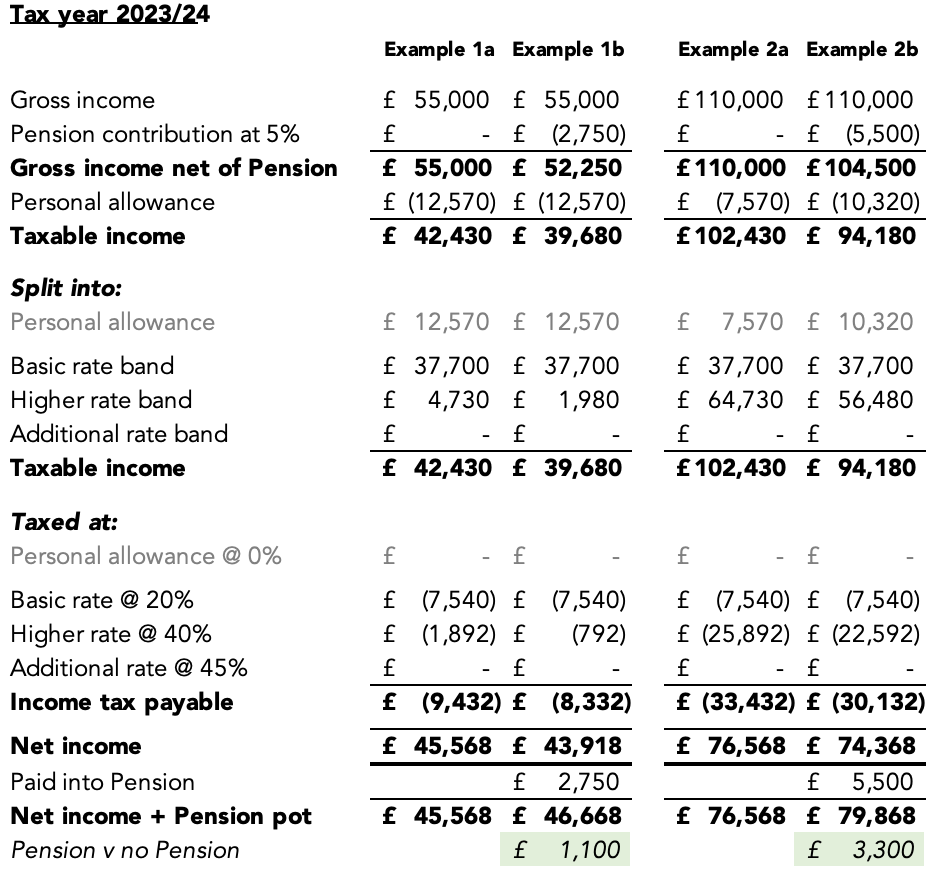

Let’s look at 2 examples of a current higher rate tax payer:

Worked Example

Notes

- See that although Net Income is lower when a Pension contribution is made, the total of Net Income plus the Pension pot is higher. This is due to the tax saving.

- Also notice the impact the Pension contribution has on the Personal Allowance in Example 2, as the Gross Income is over than £100k threshold mentioned in the Income Tax section above.

Employer contribution to your Pension

The other benefit you get with Pensions, is that your employer is legally required to contribute a minimum amount to your Pension pot.

This is currently a minimum of 3% of your earnings.

An employer may contribute more as an additional employment “perk”, for example:

- Employee Pension contribution = 5%

- Employer Pension contribution matches employee = 5%

- Total contribution = 10%.

Check with your employer what’s the best Pension contribution they can offer you.

Useful Links

Money Saving Expert‘s income tax calculator tool also lets you input your pension contribution.

See more in the Pensions section.